Volatility has increased – and even the real estate market is susceptible

Many investors look to real estate investment strategies to help diversify the risks of traditional asset classes like equities or fixed income. Yet despite its potential diversification benefits, the real estate market is still subject to volatility, which can increase during periods of economic stress. The COVID-19 pandemic has certainly spurred volatility in the real estate market, with increased unemployment, vacancies and challenges for some commercial or residential tenants to even pay rent. As of September 30, 2020, a well-known representation of the Real Estate Investment Trust (“REIT”) market, the FTSE Nareit All Equity REITs index, was down ~10.1% year-to-date1.

On the flip side, though, real estate corporate bonds were up ~7.5% year-to-date2. Taking a deeper look at the fundamental underpinnings of real estate companies, we believe that the debt they issue may represent a compelling investment opportunity.

Real estate companies look particularly attractive from a debt perspective

REITs have differentiated financial covenants compared to other investment grade fixed income sectors. These financial covenants can help the company better manage debt by limiting the amount of leverage it employs and controlling the ability of the REIT to incur too much debt, thereby potentially helping safeguard fixed income investors. They help to ensure:

- There are assets to cover debt in a worst-case scenario

- Issuers have the means to pay interest and principal at maturity

- Assets are maintained in an effort to prevent loss of value

- Transparency through disclosure

We believe the fundamental strength of U.S. REITs is relatively stable and strong. In fact, over the last twenty years, there have been virtually no historical bankruptcies for REITs with a standard covenant package. The only equity REIT to go bankrupt during the 2008 Financial Crisis was a commercial real estate investment company named General Growth Properties, Inc. (“GGP”). GGP became overextended after an extremely large acquisition of retail malls in the early 2000s. Despite the bankruptcy filing, owners of GGP corporate debt who held through the initial volatility saw their bonds return to par by 2010 due to strong sentiment about GGP’s asset base3. This is an example of how the seniority of real estate corporate bond investors have in the capital structure of REITs can help manage volatility in periods of economic stress.

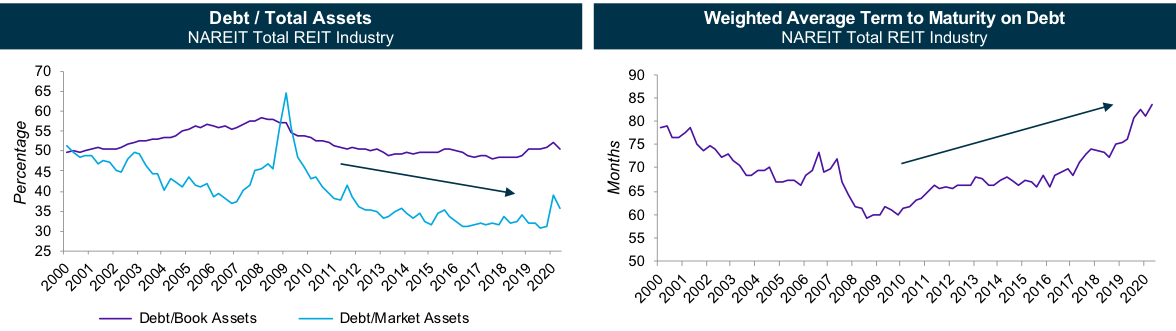

The strength of REITs' balance sheets continues to grow, as REITs have spent the last decade preparing for another downturn. Following the 2008 Financial Crisis, REITs have exhibited substantial improvement in their capital adequacy and liquidity coverage ratios, while also growing net income against a backdrop of strong real estate fundamentals and lengthening their maturity profile.

The strength of REITs' balance sheets continues to grow

Source: NAREIT T-Tracker as of June 30, 2020 Information is subject to change and is not a guarantee of results.

Increasing diversification with corporate bonds issued by real estate companies

Investors may consider complementing and diversifying their real estate equity allocations with real estate corporate bonds, or bonds issued by predominantly equity REITs. We expect that real estate corporate bonds will provide investors with similar economic exposure and diversification benefits as real estate equities, yet with less volatility and higher credit quality. Investors can now invest in a portfolio of corporate bonds issued by U.S. real estate companies with the Emles Real Estate Credit ETF (REC).

Tags: Diversification, ETF, Income, Volatility