Luxury is a uniquely resilient1 consumer segment with high growth potential. In our view, however, luxury goods’ global nature and lack of standardization of what defines “luxury” have helped prevent investors from maximizing the benefits of this unique industry to date. To address this issue, Emles has created the Global Luxury ETF (LUXE), which aims to be the first fund to provide investors access to a portfolio of what we consider 50 most representative luxury goods companies globally.

What are luxury goods and why do they merit standalone consideration?

While everyone is familiar with the concept of “luxury” brands such as Louis Vuitton and Hermès, one single definition of luxury does not exist. In academia, for example, numerous studies have attempted to describe luxury goods as satisfying certain distinct criteria, such as price, quality, aesthetics, rarity, extraordinariness, and symbolism2. Investors and every-day consumers, on the other hand, may define luxury in a myriad of ways that may drastically differ from one another.

We consider luxury goods to be a distinct consumer category for several reasons. Studies3 have found that luxury goods consumers have stronger brand loyalty than “mass-market”4 brand consumers, which indicates uniquely strong brand equity. Given that luxury companies command pricing power over mass-market brands, they have been shown to exhibit more resilient through-the-cycle margins;5 Bernard Arnault, CEO of LVMH (Louis Vuitton Moët Hennessy), has famously stated that “luxury is the only sector that can provide luxurious margins.”6 Lastly, as we discuss below, luxury consumption has also shown to be more resilient than mass-market in the aftermath of COVID-19.

Luxury goods is a resilient, high-growth consumer category

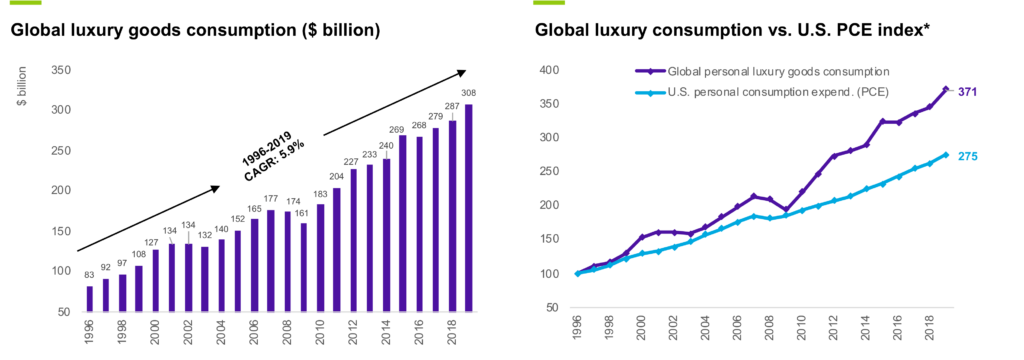

Global personal “luxury goods” consumption has grown at a CAGR of 5.9% from 1996 to 2019, reaching $308 billion in 2019. As we show in the charts below, annual growth in consumption has been steady over several economic cycles in this time period. Moreover, growth in luxury consumption has accelerated over the last decade largely due to the rise of the Chinese consumer, significantly outpacing U.S. personal consumption in the time period.

Past performance is no guarantee of future results. Note: As of December 31, 2019. *All figures are in U.S. Dollar terms; Rebased index, 1996 = 100. Global events such as the current novel coronavirus (COVID-19), terrorist attacks, natural disasters, social and political discord or debt crises and downgrades, among others, may result in market volatility and have long term effects on both the U.S. and global financial markets.

Source: Bloomberg, Visual Capitalist, Emles Advisors LLC

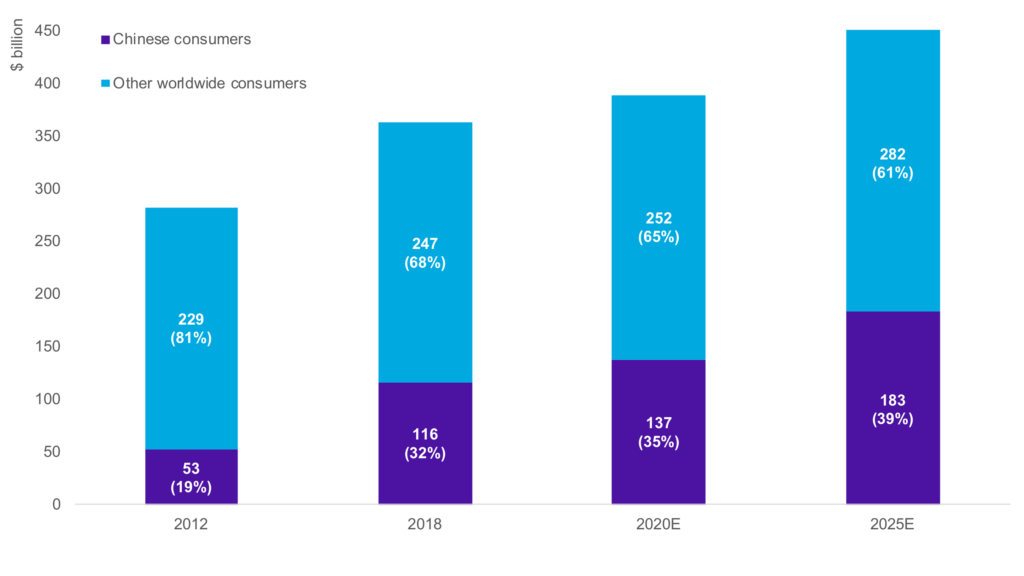

Furthermore, China’s contribution to growth in luxury goods spending is expected to increase over the next decade. According to luxury market forecasts provided by McKinsey, Chinese consumption is set to grow by 60% between 2018 and 2025E, or 65% of total industry growth (McKinsey forecasts 28% growth in aggregate luxury spending from 2018 to 2025E). LUXE can therefore also offer investors exposure to Chinese consumption growth without risks of investing directly in China.

Chinese contribution to global luxury growth, 2012 to 2025E ($ billion / % global consumption)

Information is subject to change and is not a guarantee of future results. Note: As of April 2019. Converted to U.S. Dollars from estimates in RMB; using a different source and FX assumptions vs. previous slide may cause figures to not tie exactly; E = Estimates. Past performance and industry estimated are not a guarantee of future results. Global events such as the current novel coronavirus (COVID-19), terrorist attacks, natural disasters, social and political discord or debt crises and downgrades, among others, may result in market volatility and have long term effects on both the U.S. and global financial markets.

Source: McKinsey

The sector continues to show resilience despite the overall effects of COVID, particularly in relation to other consumer segments. In the aftermath of COVID-19, for example, Q2 2020 results in China indicated that luxury goods companies’ sales rebounded more quickly than mass-market quarter-on-quarter.7 Strong financial index performance, too, has set luxury goods apart from other global consumer segments this year, particularly in the second half of 2020.

Create a more resilient equity portfolio with Emles Global Luxury ETF (LUXE)

We believe luxury goods’ investment characteristics and growth prospects create the need to carve out this unique consumer segment, in our view; investors may therefore seek to create more resilient portfolios by considering luxury goods for standalone consumer allocation. In our view, the sector offers a unique combination of high growth, strong brand equity, and increasingly higher barriers to entry, which differentiates it from other consumer segments. Market response to the COVID-19 pandemic in 2020 has further emphasized luxury goods’ unique investment characteristics. The Emles Global Luxury ETF (LUXE) aims to be the first ETF to provide access to this unique industry.